FY26 Market Return Drivers and Detractors

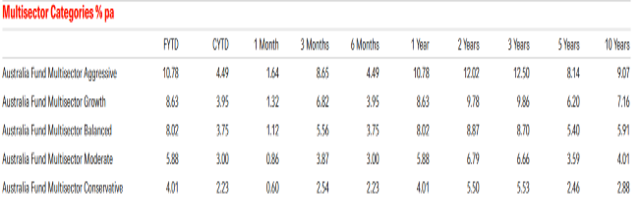

Based on Morningstar category averages FY2026 delivered positive returns across all diversified portfolios despite a mixed outcome across major asset classes. Multisector portfolios benefited from broad diversification, with risk-adjusted returns generally rewarding investors who maintained exposure to global markets during the year.

Key Contributors to FY2026 Returns

- Emerging Markets Equities

Emerging Markets was the strongest major asset class during FY2026, delivering a return of 27.20%. The category also generated a strong annualised two-year return of 20.94%, indicating consistent momentum rather than a short-lived rally. This would have been a meaningful contributor to diversified portfolios with global equity exposure.

- Asia Pacific ex-Japan Equities

Asia Pacific ex-Japan was similarly strong, returning 29.23% during FY2026. The region significantly outperformed developed market peers and provided an important diversification benefit beyond traditional US and European market exposures.

- Global Equity – Currency Hedged

Currency-hedged global equities returned 18.30%, outperforming unhedged global large blend equities (10.49%). This suggests currency movements acted as a headwind for Australian investors during the year and that hedged exposure added significant value.

- Global Infrastructure

Global Infrastructure produced a return of 13.56%, providing both growth and defensive characteristics. Infrastructure continued to deliver attractive returns with lower volatility than broader global equities, making it a valuable contributor to diversified portfolios.

- Credit Markets

Within fixed income, the strongest contributors came from credit sectors:

- Diversified Credit: 5.23%

- High Yield Credit: 5.33%

- Multi-Strategy Income: 4.87%

These returns materially exceeded traditional bond sectors and helped support Moderate and Conservative portfolios.

Key Detractors from FY2026 Returns

- Australian Growth Equities

The weakest major equity category was Australian Large Growth, which returned only 2.72% for FY2026 and just 0.76% over the most recent one-year period. This represented a significant lag relative to global growth equities and was a major drag on domestic allocations.

- Australian Broad Market Equities

Australian Large Blend equities produced only 3.20%, while Australian Large Value generated 5.97%. Although positive, these returns were well below international equity markets and likely weighed on balanced portfolios with meaningful home-market bias.

- Global Bonds

Traditional global bond exposures produced relatively modest outcomes:

- Global Bonds: 2.43%

- Australian Bonds: 1.81%

- Global/Australian Bonds: 2.84%

While bonds supported capital preservation, they contributed less to total portfolio returns compared with equities and credit.

What Drove Multisector Returns?

FY2026 reinforced the importance of diversification and global asset allocation. Multisector investors were rewarded for maintaining exposure to growth assets, particularly international equities, while defensive allocations provided stability but limited return contribution. The strongest outcomes were achieved by portfolios that combined:

- Meaningful international equity exposure.

- Allocations to higher-yielding credit sectors vs duration.

- Diversifying assets such as infrastructure.

For diversified investors, FY2026 was a year in which offshore equity exposure overwhelmingly drove returns, while Australian equities and traditional bonds acted more as stabilisers than return generators.

Copyright © 2026 Coastline Private Wealth, All rights reserved.

Our mailing address is:

PO Box 2082

Churchlands WA 6018