Over the past week, global investment markets have continued to grapple with the evolving conflict in Iran. While geopolitical events are never the sole driver of returns, this particular situation is having a tangible impact due to energy prices / oil supply.

What’s happened this week

The most important development has been the sustained disruption to oil flows through the Strait of Hormuz, a critical artery for global energy supply. Oil prices have remained elevated, with benchmarks pushing well above US$120 per barrel at times, reinforcing inflation pressures globally.

Unsurprisingly, this has created a more volatile backdrop for markets:

- Global equities have been volatile, with energy and defence sectors outperforming, while broader indices have struggled to gain direction.

- Bond markets are increasingly sensitive to inflation risks, with central banks signalling caution.

- Economic data is beginning to reflect the strain, particularly in Europe where policymakers have highlighted risks to both growth and inflation.

In short, the market narrative has shifted from “soft landing” optimism earlier this year to a more complex mix of geopolitical risk + inflation persistence.

Why this matters for investors

At its core, the Iran conflict is acting as a supply shock. Higher energy costs flow through to transport, manufacturing and consumer prices, which in turn:

- Keeps inflation higher for longer

- Central banks increase interest rates to fight inflation

- Cost of capital increases leading to lower corporate profits and less consumption

- Puts pressure on economic growth and unemployment rises

This combination raises the risk of a “stagflationary” environment - slower growth alongside elevated inflation - which markets typically find challenging.

The outlook from here

Looking ahead, there are three key scenarios to consider:

1. Prolonged disruption (base case)

The conflict continues without a clear resolution, and energy markets remain tight. Under this scenario:

- Volatility stays elevated

- Inflation declines more slowly than expected

- Central banks remain cautious

This is currently the most likely path being priced by markets.

2. Escalation scenario (risk case)

Further disruption to energy infrastructure or shipping routes could push oil prices materially higher again. This would:

- Increase recession risks, particularly in Europe and parts of Asia

- Lead to sharper equity market drawdowns

- Benefit defensive and real asset exposures

3. De-escalation (upside case)

Any credible ceasefire or reopening of supply routes would likely see:

- Oil prices fall quickly

- Equity markets rally

- Renewed confidence in a more benign inflation outlook

Importantly, markets can move quickly if expectations shift—even before the underlying situation is fully resolved.

Our approach

At present, we are not making wholesale changes based solely on geopolitical developments, but we are ensuring portfolios remain well diversified and resilient across a range of potential outcomes as well as holding a bit more cash.

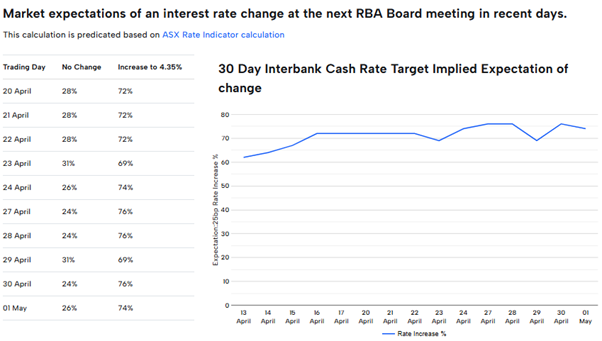

Reserve Bank of Australia – meets 5th of May 2026

As of the 1st of May, the ASX 3 Day Interbank cash rate futures May 2026 contract was trading at 95.745, indicating a 74% expectation of an interest rate increase to 4.35% at the next RBA Board meeting.

Copyright © 2026 Coastline Private Wealth, All rights reserved.

Our mailing address is:

PO Box 2082

Churchlands WA 6018